AMA Research values window and door fabrication market at £1.94 billion

New AMA report Reviews Developments in the Door and Window Fabricators Market

“In 2013, the prospects for the door and window fabrication sector are relatively pessimistic and the fragility of the economy remains a significant factor. However, early-mid 2013 has seen some tentative positive indicators with some encouraging signs in the housebuilding sector – though housemoving and household spending levels are flat, and the commercial construction market shows little sign of any significant growth in the short-medium term Gradual improvement in the medium term is anticipated, given sustained improvement in the economy, though this is dependent on the speed and timing of recovery.”

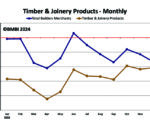

The windows and doors fabrication market has been in steady decline over the last decade, but has fallen by around 30% since 2007. At trade prices, the market in the UK was worth around £1.94 billion in 2013. Key defining factors in this market in 2013 are: market maturity (in particular for the domestic replacement market), fragmentation, competition, cost-management, building legislation, ‘green’ building, austerity and diversification.

The windows and doors fabrication market has been in steady decline over the last decade, but has fallen by around 30% since 2007. At trade prices, the market in the UK was worth around £1.94 billion in 2013. Key defining factors in this market in 2013 are: market maturity (in particular for the domestic replacement market), fragmentation, competition, cost-management, building legislation, ‘green’ building, austerity and diversification.

The development of the economy is the key driver of the glazing sector, which has been severely impacted by the recession. Issues associated with the effects of the financial crisis, such as the continuing restrictions in credit, the slump in housebuilding and the flat housemoving market, have also impacted the sector negatively.

The chart illustrates the fragmented product mix. Residential windows account for an estimated 26% of the market at trade prices, but commercial glazing is a significant sector at 17%. Curtain wall, ground floor treatments are also key sectors, though market conditions in some non-housing sector shave been just as tough as housebuilding and home improvements in 2009-12.

The supply structure remains very fragmented, comprising of vertically integrated retail glazing companies, PVC-U trade fabricators and fabricator/installers, aluminium systems fabricator/installers, bespoke glazing contractors, composite door manufacturers, commercial glazed door manufacturers, roof light manufacturers, steel window manufacturers and major joinery companies.

Closures and acquisitions/mergers continue to be a striking feature of the market in 2012/13 – across all segments within the industry – reflecting significant over-capacity particularly in PVCu fabrication. In 2013, the prospects for this industry in the immediate term remain relatively pessimistic and the fragility of the economy remains a significant factor. However, early-mid 2013 has seen some tentative positive indicators, with some encouraging signs in the housebuilding sector – but housemoving and household spending levels are flat, and the commercial construction market shows little sign of any significant growth in the short-medium term Gradual improvement in the medium term is anticipated, given sustained improvement in the economy, though this is dependent on the speed and timing of recovery. It seems likely that capacity in the window replacement market will continue to reduce along with demand, and that the already expected consolidation of this market will become more rapid as a result of current circumstances. Further mergers and acquisitions are forecast across this industry as it continues to adjust to market conditions, though the industry will still remain fragmented reflecting the differing demands of products and market application areas. Finally, the market will continue to develop in response to legislation and building regulations, which will continue to focus on ‘green’ building materials, thermal efficiency etc. AMA Research’s report “Door and Window Fabricators Market Report – UK 2013-2017 Analysis” is available in hard copy or electronic format for £675 and can be ordered online at www.amaresearch.co.ukor by calling 01242 235724.

{kind=link}